Unlocking the Puzzle: Unraveling Decreasing Compliance Despite Investment

In an era of substantial investments in data management, an intriguing paradox emerges. A recent McKinsey-IIF survey unveils that banks have poured considerable resources into data management, striving to align with BCBS 239 and other compliance benchmarks. However, an irony emerges as their own self-assessments reveal a decline in overall compliance levels since 2015. The question looms large – what underpins this unexpected trend?

Decoding Tactical Approaches

A closer examination points to a strategic dissonance. While regulatory projects have aimed to establish a strong foundation, the focus often remains on the immediate and tactical aspects. Banks have been dedicated to shoring up documentation and implementing selective remedies. Yet, in many cases, the automation of vital data governance processes remains in its infancy or is scheduled for later stages. The result? Compliance deadlines were met, but with limited scalability and reusability, constraining the ability to accommodate future demands.

Revealing the Unknown

The investment tide has not been in vain. A silver lining emerges as banks delve deeper into the nuances of compliance. Evaluations unearth previously concealed gaps, casting a spotlight on the intricacies of technical compliance requirements. The road ahead entails addressing these revelations, rectifying inadequacies that were once hidden from view.

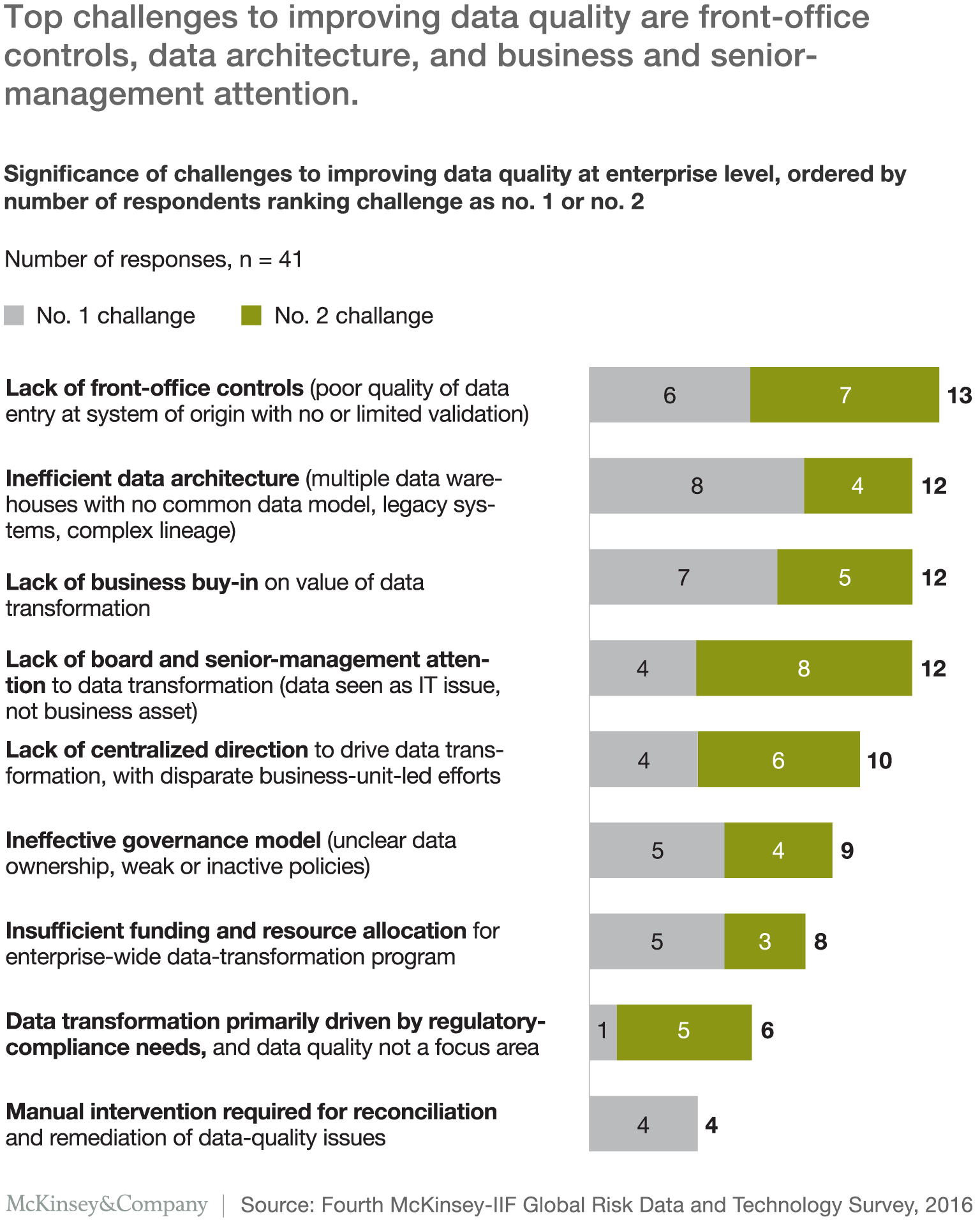

Quality Quandaries

Within this landscape, a significant challenge emerges – data quality. The survey underscores the critical role of front-office controls, highlighting how poor data quality in systems of origin can cascade into compliance complications. Moreover, the blemishes are exacerbated by suboptimal data architecture and corresponding operational inefficiencies, which ripple across numerous banks. Evidently, rectifying this dual challenge will necessitate ongoing investments over the forthcoming years.

Evolving from “Change-the-Bank” to “Run-the-Bank”

Amidst these trials, leading banks are finding rays of success within their data programs. They distinguish themselves through a triad of strategic shifts:

- Strategic Data Management: Beyond compliance, leading banks recognize data management as a strategic catalyst. Enriched customer analytics, fortified risk management, and heightened operational efficiency become the cornerstones of differentiation.

- Embedding Data Governance: Departing from mere tactical cost considerations, data governance and quality initiatives emerge as integral business enablers. Addressing data quality gaps at the source enhances operational efficiency while fortifying compliance, necessitating an active and embedded data governance approach.

- Harmonized Data Vision: A transformative shift towards harmonized data vision and strategy unfurls. This holistic approach ensures value permeates divisions and geographies. Data governance, quality processes, and advanced analytics seamlessly coalesce to empower the business’s core objectives.

As the data management landscape evolves, a noteworthy trend unfolds. The spectrum of data management investments is diversifying, propelled not solely by risk mitigation but by broader and more encompassing initiatives. In this dynamic context, banks are deciphering the intricacies of compliance, rewriting the script of investment outcomes.

Leave a comment